The fundamental economic question of "what to produce" refers to the goods and services that a society chooses to make available. This decision is based on the preferences and needs of consumers, as well as the productive capabilities of the economy. Societies must weigh tradeoffs and decide which mix of products will best satisfy the populace, taking into account factors like resource availability, production costs, and potential demand.

The "how much to produce" component of the basic economic question deals with determining the optimal quantity of each good or service to manufacture. This requires analyzing supply and demand dynamics to find the equilibrium output level that clears the market. Producing too little leads to shortages, while overproduction results in waste and inefficiency. Striking the right balance is crucial for maximizing economic welfare.

The "how to produce" aspect refers to the methods and technologies employed in the production process. Societies must decide on the optimal combination of labor, capital, natural resources, and entrepreneurship to create goods and services. Factors like productivity, cost, and environmental impact all influence these production decisions. Economies are constantly evolving as innovations allow for more efficient ways of making things.

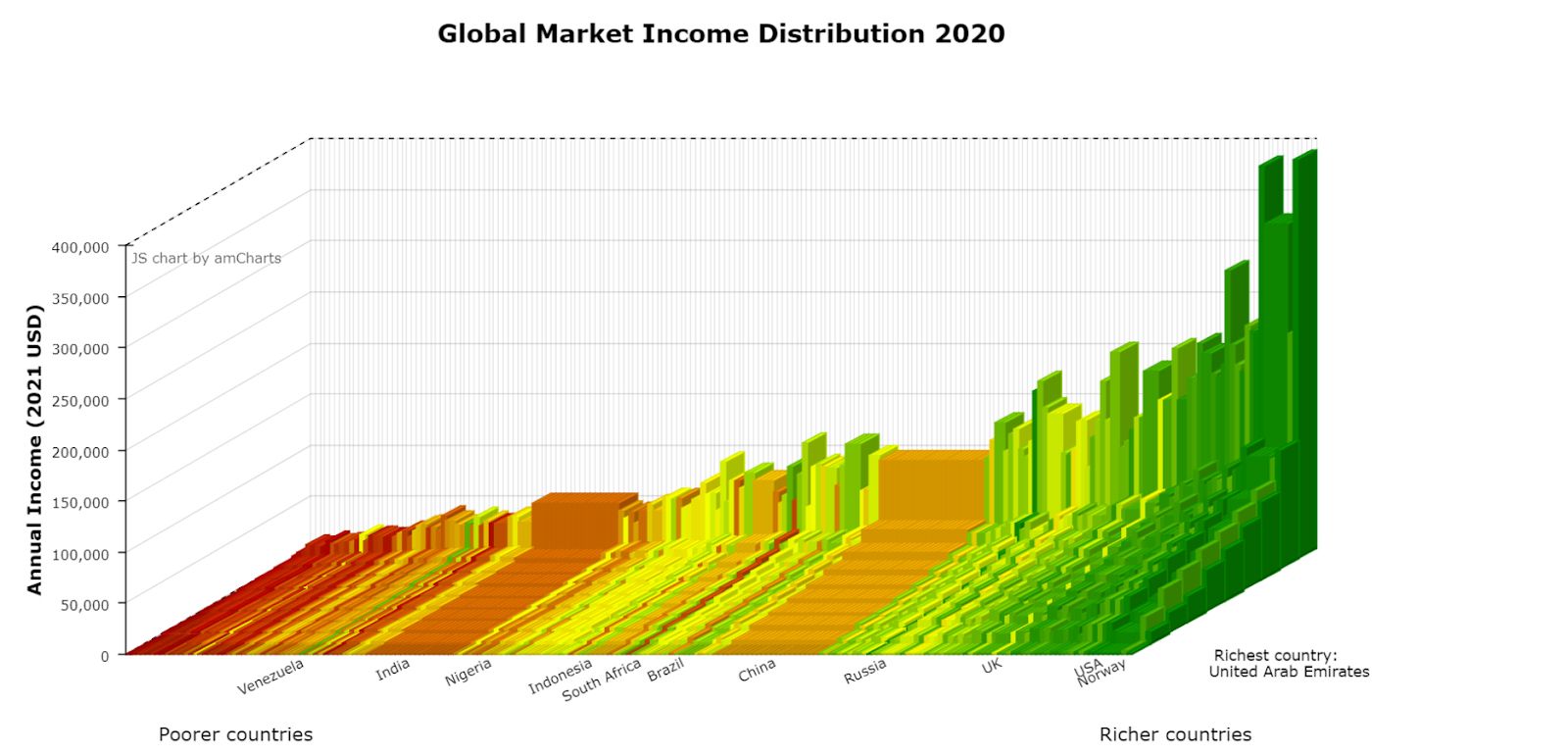

The "for whom to produce" component of the basic economic question is concerned with how the output of an economy is distributed among individuals and households. This involves considerations of income inequality, access to goods and services, and the fairness of the economic system. Governments often implement policies like taxation, social welfare programs, and regulations to shape the distribution of income and resources.

Resource Allocation and Output/Input Distribution

Resource allocation is the process by which an economy decides how to use its limited factors of production—land, labour, capital, and entrepreneurship—to satisfy society's wants and needs. Efficiently allocating these scarce resources is crucial for maximizing economic output and welfare. The distribution of this output back to the owners of the inputs (workers, landowners, capitalists, etc.) then determines the income levels of various individuals and groups. Imbalances in this distribution can lead to concerns about equity and social justice.

The "for whom to produce" aspect of the basic economic question is closely tied to the distribution of income among individuals and households. Some have high incomes from well-paid jobs or ownership of productive assets, while others struggle with low wages or unemployment. Governments often intervene to influence income distribution through tax and transfer policies, with the goal of achieving a more equitable society.

Equity, in this context, is the idea of being fair or just, It is about making sure that everyone in society has the same opportunities to succeed. It is also about creating a society where everyone has access to the same resources, regardless of their background. Equity is an important part of a fair and just society.

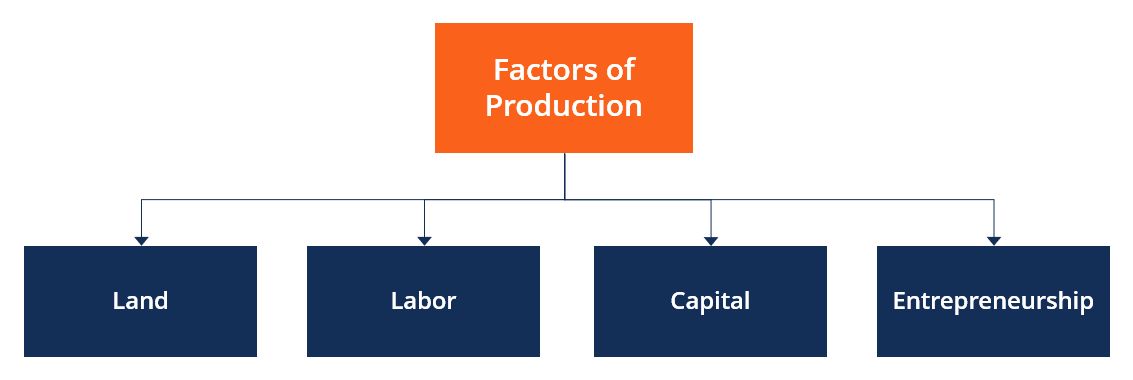

The four main factors of production are the essential inputs required for the creation of goods and services in an economy. These factors determine a society's potential to produce and the composition of its output.

Land refers to all the natural resources that are used as inputs in the production process. This includes not just arable land for agriculture, but also mineral deposits, timber, bodies of water, and other natural assets. The availability and quality of land impacts the kinds of goods and services that can be produced.

Labour encompasses the human effort, both physical and cognitive, that goes into production. This includes the skills, knowledge, and talents of workers. The size, education level, and health of the labor force are key determinants of an economy's productive capacity.

Capital consists of the manufactured goods used to facilitate production, such as machinery, tools, buildings, and infrastructure. These produced inputs amplify the productivity of land and labor, allowing for greater output. Investment in physical capital is crucial for economic growth.

Entrepreneurship is the fourth critical factor of production. Entrepreneurs are the risk-takers and innovators who organize the other factors - land, labor, and capital - in new ways to create value. Their ability to spot opportunities, marshal resources, and bring new ideas to market drives economic progress.

The term "capital" encompasses a broader range of productive assets beyond just physical equipment and structures. Economists recognize several distinct types of capital that contribute to economic activity.

Physical capital refers to the tangible, human-made goods used in production, such as factories, tools, and transportation networks. Investments in physical capital enhance productivity and expand an economy's production possibilities.

Human capital represents the skills, knowledge, and capabilities embodied in the workforce. Education, training, and health improvements all increase the quality and productivity of labour, driving economic growth.

Natural capital consists of the environmental assets and ecosystem services provided by nature, including agricultural land, mineral deposits, forests, and clean air and water. The availability and sustainable use of natural capital is crucial for long-term prosperity.

Financial capital encompasses the monetary resources available for investment, such as cash, stocks, bonds, and other financial instruments. Well-functioning financial markets channel savings into productive uses, facilitating capital accumulation.

All of these forms of capital - physical, human, natural, and financial - are essential inputs to the production process. Economies that can build up and efficiently utilize diverse forms of capital tend to achieve higher levels of output and income.

The basic economic question of "what, how much, how, and for whom to produce" is at the heart of any society's economic system. Answering these questions requires careful consideration of resource allocation, input distribution, and the various factors of production. By understanding these core economic concepts, policymakers and citizens can work towards an economic system that efficiently and equitably satisfies the needs and wants of the population.

Stay up to date with the our progress, announcements and exclusive tips. Feel free to sign up with your email.